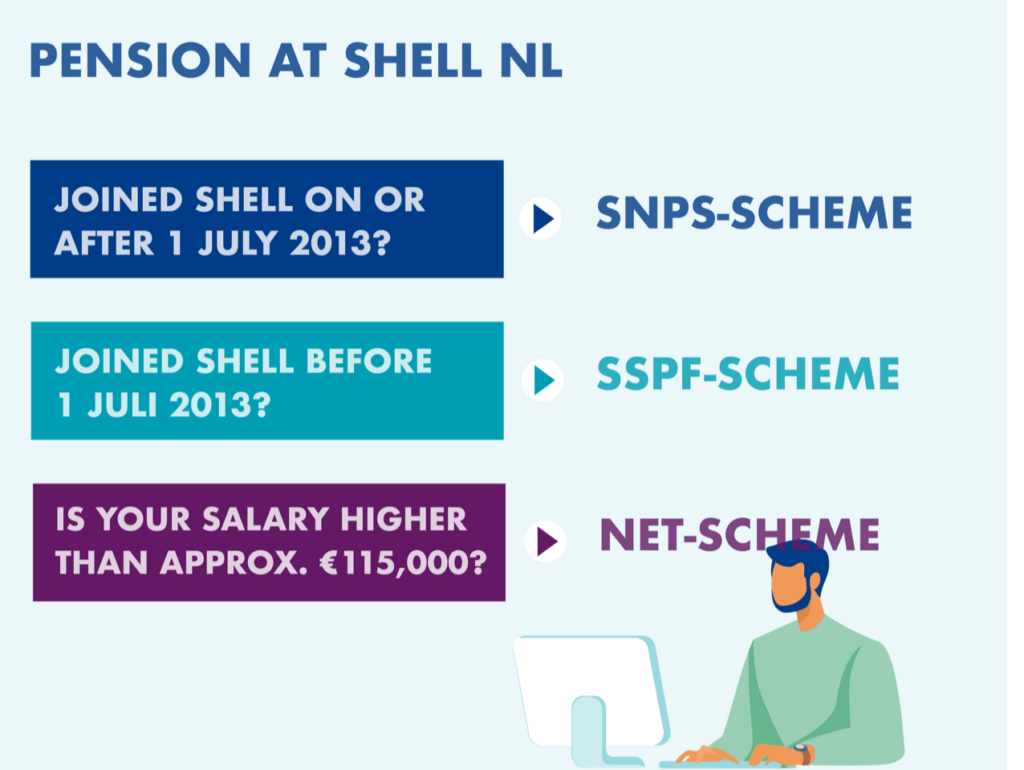

Currently you accrue a pension with at least one of Shell’s two pension funds. Shell has two different basic pension schemes:

The government, employers and employees have made agreements in the Pension Agreement of 2019 about what the new pension system in the Netherlands should look like. The changes affect almost everyone. These agreements have been incorporated into a new law, the Future Pensions act.

The deadline for switching to a new pension scheme is 1 January 2028. That is why Shell is currently working together with the Central Works Council on a new pension scheme for Shell employees in the Netherlands (Shell NL). It is our intention to transfer the current employees in the SNPS scheme to the new pension scheme as of 1 January 2025. The changes for this group are limited as the SNPS scheme is already a premium scheme. The participants in the SSPF scheme will transfer a year later because more time is needed to transfer the employees in the SSPF pension scheme. Would you like to know more about why we have to switch to a new pension system? Then please read on.

The Future Pensions Act contains a number of agreements that should ensure that more people accrue a pension that maintains purchasing power. We explain the most important agreements:

The transition to the new pension scheme mainly affects employees who are currently accruing pension in the SSPF scheme. This is the scheme for employees who were employed before 1 July 2013. The other pension scheme, the SNPS scheme, is already a premium scheme. But that pension scheme will also need to change slightly as well. Please make your choice below.

At Shell, we have two types of pension schemes and, depending on when you joined the company. Read more on this below.

The Central Staff Council has a right to consent with respect to a proposed amendment to the pension agreement between the employer and the employee. As soon as there is a proposed decision the Central Staff Council will be asked for consent. The Central Staff Council has established a Pension Committee with specific knowledge on pensions.

We believe that proper consultation is very important and therefore regularly consult both the Pension Committee and the Central Staff Council regarding the developments. In these discussions, we have shared a lot of knowledge and we looked at the changes that the WTP prescribes, the possibilities that exist and what that will mean for Shell.

We expect the process of formal consultation with the Central Staff Council to start around the summer of 2023. Concrete proposals will be discussed. During this process, the VOEKS hearing rights committee will also be involved. They may give an opinion on the transition plan. All this will eventually lead to a proposed decision that will be submitted to the Central Staff Council for approval.

We are busy mapping out the consequences and analyzing the various possibilities. This will be the basis for the discussions with the Central Staff Council (COR) and VOEKS and of course also with the pension funds. This will ultimately lead to a proposed decision which will be submitted to the COR for approval. It will describe the consequences for various age groups. This decision then will be shared with the pension funds for further decision-making and implementation. In the case of the pension funds, the accountability body has a role in the decision-making process. Although more and more is becoming clear, it will not yet be known what the exact changes will be on an individual level. It will become more clear during the implementation process by the pension fund. Given the implementation period that the government has in mind (somewhere between 2023 and 2028), this may take some time. We will keep you informed via the website.

Pensions is, and will remain, an important condition of employment for Shell. We realise that our pension will have to change in line with developments in the Netherlands and that will have consequences for existing employees. In making the changes we will also look at possible improvements in the schemes. We think that offering choices to employees (including a good default if you do not want to make choices), clarity and transparency, are important features in developing the new pension scheme. Furthermore, we value good communication and providing opportunities to improve insight into your financial situation after retirement.

That is not yet known. Under the new premium contribution scheme, a certain level of pension contribution will be paid on a monthly basis. The contribution will be subject to a fiscal maximum.

Each company will have to set a defined pension contribution within the fiscal limits, and the level of employer and employee contributions and possible choices. This is part of the many aspects that will have to be discussed with the Central Staff Council.

The longer you work, the more pension you accrue. Furthermore, the value of your accrued pension will, in principle, be retained. Even if this accrued value were to be converted into the new pension scheme, this would not only apply to the pension you have already accrued but also to all pensions in payment. Early retirement would not prevent that.

There may also be other reasons for you to retire early. If you would like to discuss this option, please contact Achmea Pension Services.

Good communication is important for the success of this transition. “Winning hearts and minds” is our motto. Our aim is for people to trust Shell’s good intentions and in the process we have gone through together.

Therefore this website has been developed: “The new pension at Shell”. Everyone (current and former employees) can go to this website for information. All the information provided is available to everyone. You will also see an interactive timeline on the platform, so that it is clear where we stand in the process. Now the new legislation has been approved by the Senate, a process of decision-making and consultation by Shell NL, the Central Staff Council and the Pension Funds will follow. It will take a while before the individual consequences will be known exactly. Nevertheless, we would like to keep you informed of the developments via the website.

In 2023 and 2024, we held several information sessions where we covered the changes, the main choices we need to make and where we are in the process.

Pension is a complex subject and that makes communication about it a challenge. By using various tools, we want to explain the changes and the process to you in a simple manner. We will also consider the information access of the various participants. The primary information channel is the website, but in addition, information sessions will also be organized, and we will use info graphics, videos, and other media channels. As soon as the individual consequences are known, you will be informed individually by the pension fund. If you want to know more about your current pension, you can visit the website of the pension fund (www.shellpensioen.nl). You can also view your own pension online via www.shellpensioen.nl/my pension. Log in with your DigiD.

You can contact the project group via this contact form. However, we can not answer individual questions about what exactly the changes mean for your pension at this moment. After the consultation with the COR has been completed and a new pension scheme has been agreed, the pension fund will inform you at any point about what it will mean for your own pension. Do you still have questions for the project team? If so, please fill in the contact form.

If you have any questions about your current pension or pension benefit, you can ask the Pension Fund. The Pension Fund can be reached on working days from 8.30 a.m. to 5 p.m. at +31 (0)88 462 34 56.

This is a joint website of Shell Netherlands and the Dutch Shell Pension Funds. This website is intended to inform all participants about the changes to our pension scheme as a result of the new ‘Future Pensions Act’. You cannot derive any rights from this website or from any content on this website. You can only derive rights from the pension scheme regulations applicable to you.

We use cookies on our website. A cookie is a file on your computer that remembers what you do on our website. We use these cookies, for example, to improve the website and (depending on the cookies you accept) to see what you do and view on our website.